To thoroughly implement the Accounting Standards for Business Enterprises, address issues arising in their implementation, and at the same time achieve the continuous convergence and equivalence of the Accounting Standards for Business Enterprises, the Ministry of Finance has formulated and issued Interpretation No. 15 of the Accounting Standards for Business Enterprises, which includes the following contents:

-

"Accounting Treatment for Enterprises Selling Products or By-products Produced Before Fixed Assets Reach the Intended Use State or During the R&D Process" -

"Judgment on Onerous Contracts"

The above contents shall come into force on January 1, 2022;

-

The content of "Presentation Related to Centralized Fund Management" shall come into force on the date of promulgation (December 30, 2021).

I. Accounting Treatment for Enterprises Selling Products or By-products Produced Before Fixed Assets Reach the Intended Use State or During the R&D Process

The International Accounting Standards Board (IASB) issued "Amendments to IAS 16 - Property, Plant and Equipment" in May 2020, which came into effect on January 1, 2022. In accordance with these amendments, before an item of property, plant and equipment reaches the intended use state, an enterprise shall not offset the revenue from selling products produced by the construction-in-progress (for example, revenue from selling products produced during the trial operation of construction-in-progress) against the asset cost, but shall recognize the sales revenue and costs of these trial-run products in profit or loss.

To maintain continuous convergence and equivalence with International Financial Reporting Standards (IFRS), the Ministry of Finance introduced similar provisions in Interpretation No. 15. However, it is worth noting that the trial-run sales mentioned in Interpretation No. 15 include not only the external sale of products or by-products produced before fixed assets reach the intended use state, but alsothe external sale of products or by-products produced during the R&D process.

【Luheng's Perspective】

In accordance with the provisions of Interpretation No. 15, an enterprise shall recognize the relevant revenue and costs from the external sale of products or by-products produced before fixed assets reach the intended use state or during the R&D process incurrent profit or loss:

-

If the trial-run sales are part of the enterprise's ordinary activities, they shall be presented in the items of "Operating Revenue" and "Operating Costs"; -

If they are non-ordinary activities, they shall be presented in items such as "Gain on Disposal of Assets".

It is not allowed to offset the relevant revenue from trial-run sales against the costs and then deduct the net amount from the fixed asset cost or R&D expenditure.

Before the relevant products or by-products from trial runs are sold externally, they shall be recognized asinventories or other relevant assets, and the enterprise shall disclose information such as important accounting estimates adopted in determining the relevant costs of trial-run sales in the notes to the financial statements.

Interpretation No. 15 specifically states:

-

The "products or by-products produced before fixed assets reach the intended use state" as mentioned in these provisions include samples produced when testing whether the fixed assets can operate normally; -

The "testing whether the fixed assets can operate normally" as mentioned in these provisions refers to activities to assess whether the technical and physical performance of the fixed assets meets the standards for producing products, providing services, leasing externally or being used for management, whichdoes not include assessing the financial performance of the fixed assets.

Implementation Requirements: These provisions shall come into force on January 1, 2022, and shall beretrospectively adjusted from the beginning of the earliest period presented in the financial statements for the first implementation of this Interpretation.

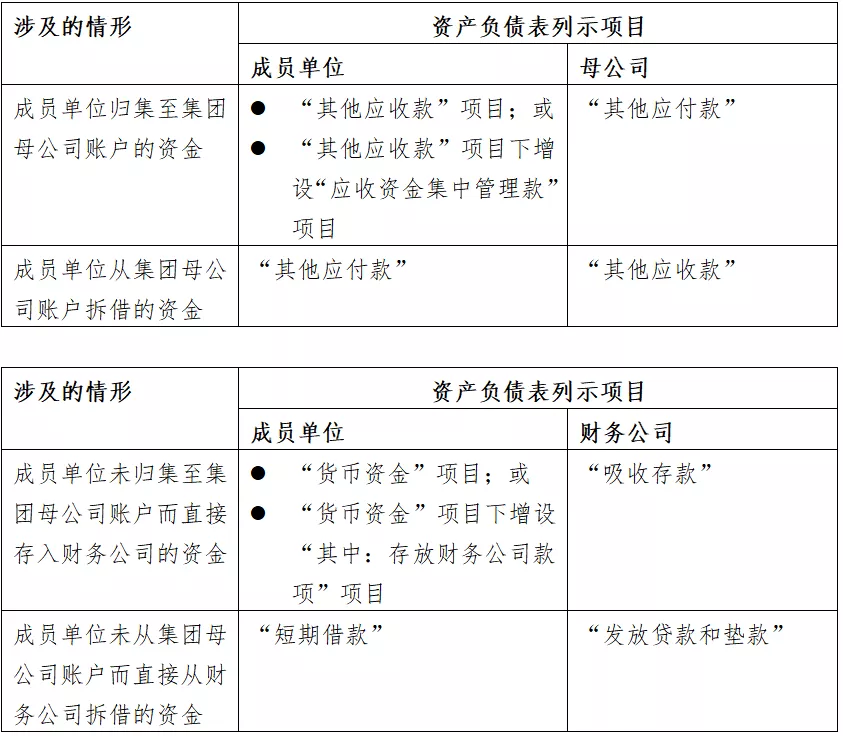

II. Presentation Related to Centralized Fund Management

Interpretation No. 15 has clearly specified how the balances involved in the centralized and unified management of funds of the parent company and its member units by enterprises through internal settlement centers, financial companies, etc., should be presented and disclosed in the balance sheet.

【Luheng's Perspective】

Interpretation No. 15 specifically explains that the above-mentionedfinancial companies refer to non-bank financial institutions that are legally subject to the supervision and administration of the China Banking and Insurance Regulatory Commission (CBIRC), established for the purpose of strengthening the centralized fund management of enterprise groups and improving the efficiency of fund use of enterprise groups, and providing financial management services for member units of enterprise groups.

Key Presentation Requirements:

-

For non-current items involved in centralized fund management, they shall be presented separately incurrent assets and non-current assets, current liabilities and non-current liabilities in accordance with the requirements for presentation by liquidity; -

In the balance sheets of the group's parent company, member units and financial companies, the relevant financial asset and financial liability items from centralized fund management shallnot be offset against each other if theydo not meet the offset criteria for financial assets and financial liabilities.

Implementation Requirements: These provisions shall come into force on the date of promulgation (December 30, 2021) and shall beretrospectively adjusted to the comparative periods, meaning that these provisions need to be applied when preparing the 2021 annual financial statements.

III. Judgment on Onerous Contracts

The International Accounting Standards Board (IASB) issued "Onerous Contracts - Costs of Fulfilling a Contract" (Amendments to IAS 37 - Provisions, Contingent Liabilities and Contingent Assets) in May 2020, which came into effect on January 1, 2022. The amendments clarified the scope of the cost concept used in judging onerous contracts. To maintain continuous convergence and equivalence with IFRS, the Ministry of Finance introduced the above-mentioned provisions of IFRS in Interpretation No. 15.

【Luheng's Perspective】

Interpretation No. 15 clarifies that the "costs of fulfilling the contract" considered by an enterprise when judging whether a contract constitutes an onerous contract shall befull-caliber costs, i.e., they shall include both:

-

Incremental costs of fulfilling the contract (direct labor, direct materials, etc.) -

Allocated amounts of other costs directly related to the fulfillment of the contract (such as allocated amounts of depreciation expenses of fixed assets used to fulfill the contract)

Rather thanonly including incremental costs.

Implementation Requirements:

-

These provisions shall come into force on January 1, 2022; -

These provisions shall be applied to contracts for which all obligations have not been fulfilled by the time of the first implementation of this Interpretation; -

The cumulative effect shall adjust the retained earnings at the beginning of the year of the first implementation of this Interpretation and other relevant items in the financial statements, andshall not adjust the data of the prior comparative financial statements.

To thoroughly implement the Accounting Standards for Business Enterprises, address issues arising in their implementation, and at the same time achieve the continuous convergence and equivalence of the Accounting Standards for Business Enterprises, the Ministry of Finance has formulated and issued Interpretation No. 15 of the Accounting Standards for Business Enterprises, which includes the following contents:

-

"Accounting Treatment for Enterprises Selling Products or By-products Produced Before Fixed Assets Reach the Intended Use State or During the R&D Process" -

"Judgment on Onerous Contracts"

The above contents shall come into force on January 1, 2022;

-

The content of "Presentation Related to Centralized Fund Management" shall come into force on the date of promulgation (December 30, 2021).

-

- What have we all Experienced in 2025

Standing at the intersection of the conclusion of the 14th Five-Year Plan and the start of the 15th Five-Year Plan, 2025 outlines the future with the brush of the rule of law. The Fourth Plenary Session of the 20th Central Committee of the Communist Party of China set the tone for the next five years, the official implementation of the Private Economy Promotion Law has given private enterprises a "reassurance pill", and the Public Security Administration Punishment Law has undergone its first major revision in nearly 20 years.212026-01 -

- Interpretation of the Building Law of the People's Republic of China

Legal Provisions:Article 19: Construction projects shall be awarded through bidding in accordance with law, and direct contracting may be adopted for those not suitable for bidding.312025-03