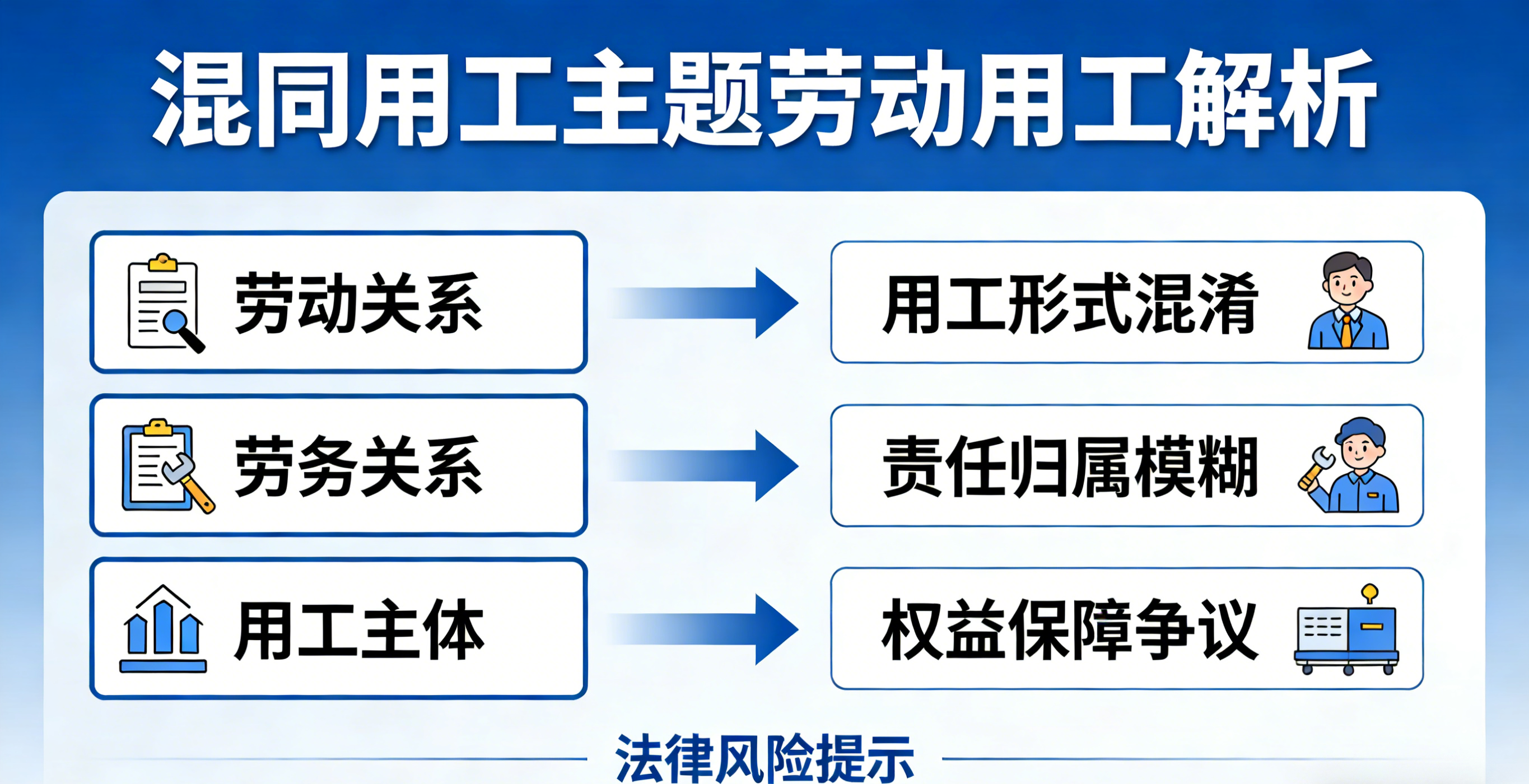

In the operation of enterprise groups, it is not uncommon for multiple affiliated companies to share office space, management personnel and employees. Although this "two brands, one set of people" employment model reduces management costs in the short term, it blurs the basic boundaries of labor relations. Workers are managed by multiple companies at the same time, and payroll, social security payment, and attendance records are completed by different entities. This paper systematically analyzes the problem of mixed employment from four dimensions: legal definition, judicial determination standards, typical risk scenarios and compliance control paths.

1. Legal definition and basis of responsibility for mixed employment

Mixed employment is not a strict legal term, but a general description of a type of employment phenomenon. Its core feature is that there is a high degree of confusion in personnel, business, finance, management and other aspects of multiple legally independent employers in actual operation, resulting in the ambiguity of the ownership of the labor relationship between workers.

At the level of legal basis, the liability for mixed employment mainly invokes the legal personality denial system and its extended application in the field of labor disputes.

-

Basis for determining personality mixing: According to Articles 21 and 216 of the Company Law, if there is a controlling or significant influence relationship between affiliated companies, and there is a high degree of confusion in terms of finance, business, personnel, etc., it can be recognized as personality mixing. -

Liability rules for denial of legal personality: Article 83 of the Civil Code and Article 10 of the Minutes of the National Conference on Civil and Commercial Trials of Courts ("Nine People's Minutes") further clarify that if a company's shareholders abuse the company's independent status as a legal person and the limited liability of shareholders to harm the interests of creditors, they shall be jointly and severally liable for the company's debts. -

Extended application in the field of labor disputes: Although the above rules were originally applied to commercial debts, the courts have extended them to the field of labor disputes in judicial practice. When workers are damaged due to wage arrears, work-related injury compensation, and other labor rights and interests, if they can provide evidence to prove that there is personality mixing in multiple affiliated companies, they can claim that these companies are jointly and severally liable in accordance with the law.

2. Judicial determination standards for mixed employment

When dealing with mixed employment disputes, courts generally adopt the review standard of substance over form, rather than simply confirming the employer based on the business license of the legal person of the enterprise. The following factors can be used as reference indicators for identifying mixed employment:

-

First, the confusion at the level of control. Many companies have common legal representatives, actual controllers or controlling shareholders, and there is a cross-appointment situation in management. -

Second, the confusion at the management level. The office space is shared and there is no clear physical distinction, managers are cross-appointed, there is a lack of independent procedures for business decision-making, and workers accept management instructions and work arrangements from multiple companies at the same time in actual work. -

Third, the confusion at the financial level. The financial accounts cannot be clearly distinguished, the financial records are not made between the companies, and the payroll payment entity is inconsistent with the social security payment entity, and there is no reasonable explanation. -

Fourth, the confusion at the personnel management level. Workers are uniformly recruited by the group and assigned to each company, and the labor contract signing entity is separated from the actual management entity, and employment management behaviors such as attendance records and performance appraisal are implemented by multiple entities.

If there are more than one of the above elements, the court will most likely find that it constitutes mixed employment. It should be noted that the identification of mixed employment does not require all elements to be present at the same time, and the key is to judge whether the enterprise has lost its independent intention and independent property.

3. Typical judicial cases of mixed employment

Company A and Company B are affiliated enterprises, and both sides share the same factory area and the same set of management teams. Workers are uniformly recruited by the group and assigned to the two companies for rotational work, wages are paid alternately by the two companies, and social security is paid by Company A. Later, when a worker was injured at work and applied for work-related injury recognition and claimed relevant benefits, companies A and B shirked each other and denied that they were the actual employers.

After trial, the court found that there was obvious confusion between the two companies in personnel management, business operations, financial income and expenditure, etc., which constituted personality confusion. In the end, it was ruled that companies A and B were jointly and severally liable for the work-related injury treatment of the worker. This case shows that in the case of mixed employment, it is difficult for affiliated companies to avoid the main responsibility of employment through mutual shirk.

4. Multiple compliance risks caused by mixed employment

Mixed employment not only leads to disputes over labor relationship determination and joint and several liability, but may also lead to broader compliance risks.

In addition to the above-mentioned labor relationship determination disputes and joint and several liability, the irregular employment model of "two brands, one set of people" will also expose enterprises to risks in social security, taxation, capital market compliance and other aspects, as follows:

-

Social security compliance risks: If the social security payer is inconsistent with the actual employer, which directly violates the provisions of Article 10 of the Social Insurance Law, "the employer shall pay social insurance premiums for its employees", the enterprise may face civil liability for social security supplementary payment and late payment penalty, and may also be subject to administrative penalties by the social security administrative department. -

Tax risk: Paying wages to workers through the spin-off of different companies may be recognized by the tax authorities as evading the obligation of individual income tax withholding and payment, constituting tax evasion, and the enterprise will face tax recovery, late payment fines and fines, and the relevant responsible persons may also bear administrative or even criminal liability. -

Audit and listing compliance risks: If a company has a financing or listing plan, the situation of mixed employment will become a major flaw in due diligence, which will not only affect the audit conclusion of intermediaries, but also reduce the recognition of enterprises in the capital market, and directly hinder the financing and listing process.

5. Practical suggestions for risk prevention of mixed employment

In order to avoid various legal and compliance risks brought about by mixed employment, affiliated enterprises need to standardize employment behavior from the aspects of definition of employment subjects, personnel management, financial operations, and cross-company collaboration.

-

Establish a single labor relationship entity: Clarify that the employee only establishes a formal labor relationship with one legal entity, and clearly and specifically stipulate the work location, direct management entity, salary payer and social security payer in the labor contract, so as to eliminate the situation of "multiple management" from the source. -

Realize the independence of personnel management: Each affiliated company needs to independently set up a human resources management department or position to independently complete the whole process of employment management such as recruitment, onboarding, attendance, salary accounting, and resignation. -

Prohibit payroll payment and mixed accounts: Strictly follow the principle of "who employs, pays, pays, and participates", strictly prohibits the payment of wages to workers through non-employers, and prohibits companies from using shared bank accounts to pay salaries, so as to ensure that the subjects of payroll, individual tax withholding, and social security payment are completely consistent with those of employers. -

Standardize the cross-company collaboration mechanism: For situations where it is necessary to arrange cross-company cooperation of workers due to business needs, enterprises should clarify the management ownership, specific job responsibilities, performance appraisal standards and salary payment methods of workers within a specific period through written "Business Power of Attorney" and "Temporary Work Arrangement Agreement" to avoid the formation of long-term and factual mixed employment.

Legal guidance

-

Article 83 of the Civil Code: "The contributors of for-profit legal persons shall not abuse the rights of the contributors to harm the interests of the legal person or other investors; If the rights of the investor are abused and cause losses to the legal person or other investors, they shall bear civil liability in accordance with law. The investors of for-profit legal persons shall not abuse the independent status of legal persons and the limited liability of investors to harm the interests of creditors of legal persons; If the independent status of the legal person and the limited liability of the investor are abused, evade debts, and seriously harm the interests of the creditors of the legal person, they shall be jointly and severally liable for the debts of the legal person. ” -

Article 21 of the Company Law: "Shareholders of a company shall abide by laws, administrative regulations and articles of association, exercise their shareholder rights in accordance with the law, and shall not abuse their rights to harm the interests of the company or other shareholders." If a shareholder of a company abuses its shareholder rights to cause losses to the company or other shareholders, it shall be liable for compensation. Article 265 (4): "Related relationship refers to the relationship between the controlling shareholder, actual controller, director, supervisor, and senior management of the company and the enterprise directly or indirectly controlled by the company, as well as other relationships that may lead to the transfer of the company's interests." However, state-controlled enterprises are not only related because they are controlled by the state. ” -

Article 10 of the Minutes of the National Conference on Civil and Commercial Trials of Courts ("Minutes of the Nine People"): "[Personality Mixing] The most fundamental criterion for determining whether there is confusion between the personality of the company and the personality of shareholders is whether the company has independent intentions and independent property, and the most important manifestation is whether the company's property is mixed with the property of shareholders and cannot be distinguished. When determining whether there is a personality mix, the following factors should be comprehensively considered: (1) Shareholders use the company's funds or property without compensation without financial records; (2) The shareholder uses the company's funds to repay the debts of the shareholders, or uses the company's funds for the free use of the affiliated company without financial records; (3) The company's account books are inseparable from the shareholders' account books, making the company's property indistinguishable from the shareholders' property; (4) The shareholder's own income is indistinguishable from the company's profits, resulting in unclear interests of both parties; (5) The company's property is recorded in the name of the shareholder, and is occupied and used by the shareholder; (6) Other situations of personality mixing. In the case of personality mixing, the following confusion often occurs at the same time: the company's business and the shareholder's business are mixed; the company's employees are mixed with shareholders' employees, especially financial personnel; The domicile of the company is confused with the domicile of shareholders. When the people's court hears a case, the key is to examine whether it constitutes personality mixing, and does not require other aspects of mixing at the same time, which is often just a reinforcement of personality mixing. ”

-

- Studying 627 Labor Dispute Cases, I Found the Three Most Dangerous Employment Methods for Enterprises

Many bosses think: Labor disputes occur by chance. But when I systematically studied 627 labor dispute cases (second-instance judgments), I found a very cruel fact:The vast majority of companies lose lawsuits not because the law is complicated, but because they have used some high-risk employment methods for a long time.162026-03 -

- Enterprise Probationary Compliance Employment Guidebook Manual

The probationary period is a key inspection period in the initial stage of labor relations, and its legal regulation not only gives enterprises the right to inspect the suitability of employees, but also sets strict boundary requirements.102026-02